Warren Buffett has always said that if an investment needs complex valuations and forecasts, it isn’t a no brainer, and he’s in the business of no brainers.

I’m paraphrasing there, but he’s explained numerous investments in that manner: there was no complex math, he was clearly getting a great deal, so he bought in.

His PetroChina investment springs to mind, this was an investment where he didn’t speak to management, he didn’t attend any presentations, he didn’t do a DCF. He just read the annual report, used judgment, and concluded it was too cheap.

Not much had to go right for him to make money. And he madea lot of money.

I love a good Buffett story as much as the next guy, but there’s a big difference between listening and understanding something. Today’s article is an exploration into the reasons why simplicity is better than other, more complex strategies.

Writing this article shifted my perspective, it can do the same for you.

Today’s sections:

The Mathematics Behind Our Forecasts

My Kinda Business

Put down the crystal ball, pick up the 10K

This is a game of probability

The Mathematics Behind Our Forecasts

How often do you think about the underlying mathematics behind your predictions? Or how many scenarios must unfold for a forecast to succeed?

Let’s say you forecast 15% revenue growth for the next three years, take a moment to think about what is required for revenue to grow 15% p.a for three years:

Finding motivated staff,

buildings in prime locations,

continued demand,

machinery,

price increases,

positive broader economy,

interest rates,

inflation, and so forth…

It’s a lot.

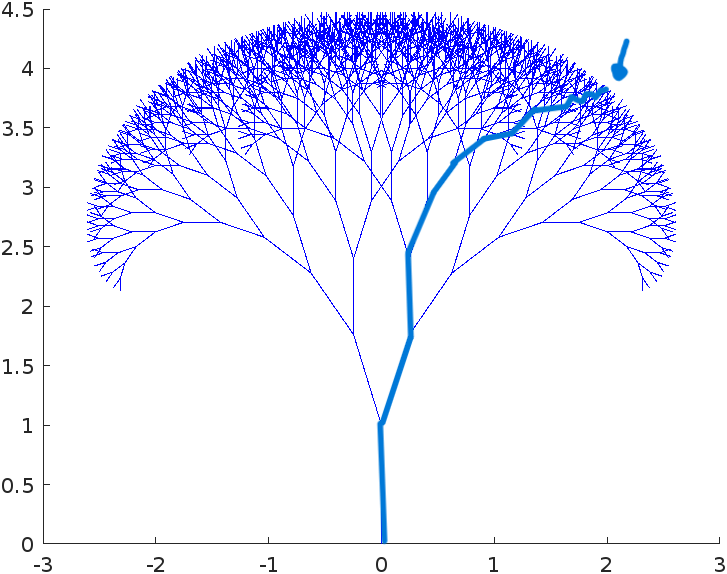

This leads to weak forecasting accuracy; each prediction depends on a chains of events, each with multiple possible outcomes, and when you predict something three years out, you’re betting that (at least) hundreds of conditional events will unfold in specific ways.

Three years from now your prediction relies on an enormous chain where each scenario branches and multiplies the possible paths reality could take. For a three-year prediction to be correct, you need to have guessed the right path through a maze of possibilities.

As we produce longer, more complex forecasts, the probability of success runs away.

Let’s look at an example: coin tosses.

How likely is it to accurately predict 10 coin tosses in a row? Presuming each individual coin toss has a 50% chance of success.

What isn’t intuitive about forecasting is that probabilities multiply, they don’t add. If you predict one coin toss, you have a 50% chance of being right. But if you need to predict two tosses correctly in a row:

50% × 50% = 25% chance

For ten tosses in a row?

0.5^10 = 0.0976% chance

That’s roughly 1 in 1,000

When you make a prediction about the future, you’re predicting a chain of conditional outcomes, like coin tosses in a row, but with more complexity. The math is unforgiving, even if each individual step seems likely, say 70% probable, by the time you string together 10 events:

0.7^10 = 2.8% chance of getting all 10 correct

Unlike coin tosses, real life outcomes aren’t binary, there are hundreds of possible outcomes at each stage, and when investing we’re often - and unknowingly - betting our hard earned money on situations with a much lower probability than that of a coin toss.

Add in the fact that black swan events could blow the entire thing up; the CEO could die in a car accident, the product could be recalled, interest rates could rise, or war could break out.

And the cherry on top? If you want to make money in the stock market, you have to disagree with it. It’s no good thinking revenue is going to grow 15% if that’s in the price already. The money is made when you think revenue is going to grow by 15% when the market thinks it’ll be 5%.

If you’re as good at forecasting as consensus, your potential for outperformance is nil.

This excerpt from a 2003 memo written by Howard Marks really drills home the point. It’s in regard to macro forecasts, but even a company specific forecast will have macro bets embedded within it. Not being aware of this doesn’t mean it isn’t there, the macro must behave accordingly if the micro is to work. This is what Marks has to say:

If you make a conventional, status quo-type forecast, you’re likely to be right most of the time.

But since the status quo usually is shared widely and factored into prices, a status quo forecast won’t help you beat the market or call its turns (even if it’s right).

The forecasts with real profit potential are the ones that correctly predict unusual events.

But idiosyncratic forecasts are wrong most of the time (and thereby unlikely to be profitable).

So if (a) conventional forecasts are easy to make correctly but generally lack profit potential, and (b) unconventional forecasts have theoretical profit potential but are hard to make correctly, then (c) it should be clear that forecasts are unlikely to help you know enough about the future to beat the market.

This chain of reasoning made me fundamentally understand that being a good investor is hard, and since studying probabilities, it’s clear that adding complex forecasts stack the odds even further against us.

So, how might we approach investing with all of that in mind? Let’s have a look at a few ideas.

My Kinda Business

In investing, you don’t get extra points for complexity. Simplicity might even get extra points because you’re not tricking yourself into thinking you know and control more than you do. When I analyse a company, I think to myself:

why risk being wrong in understanding a complex business when you can be right in understanding a simple one?

It’s pretty hard to argue with this. In a recent blog on probabilistic thinking, I spoke about a concept called calibration. Calibration is a term that explains how well someone’s subjective estimates align with the truth. If I’m on average 70% confident in my choices, I’d need to be right 7 times out of 10 to be well-calibrated.

And the beauty of a simple opportunity is that you get a better grasp on reality. Your degree of confidence, your estimates, they’re all going to be closer to reality when you actually understand the aspects of that reality.

The money I’ve lost has always been in stocks I thought I understood, but didn’t. My picture of reality was different from the truth because my understanding wasn’t what I thought it was. When you understand the business, your forecasts will correlate much closer to the truth; in essence, you stop fooling yourself and you become well-calibrated.

Looking at simple businesses, using simpler valuations, it doesn’t feel smart, but it may be the smartest thing you can do; you’re embracing what you don’t know. This is at least the case for me and my current level of knowledge.

I especially like this passage from one of Howard Marks’ 1993 memos:

None of the forecasters attempts to capture the swings (of the market) have any value unless his or her predictions are right… But it’s hard to be right.

I agree with John Kenneth Galbraith. He said “we have two classes of forecasters: Those who don’t know — and those who don’t know they don’t know.”

Put down the crystal ball, pick up the 10K

Instead of predicting the complex future, maybe it’s best to learn how to understand the present more effectively. The future is unknowable and subject to randomness. The present is true, observable, and knowable. The simpler option would be to improve our ability to analyse instead of predict tomorrow. This is a personal opinion and there are many ways to get from A to B, but my belief is that:

it is hard to predict consistently which company is going to be a long term winner,

it is easier to figure out a value for a company, and compare it to the market price.

Those who are against forecasts are more likely to be bargain hunters as it doesn’t rely on being correct about an uncertain future — only more correct about the today than others.

This is where we find the separation between value and growth investing, or as Howard Marks calls it: value today or value tomorrow investing. Those who understand how difficult it is to predict the future will tend to fall into the value today camp, where the thesis’ rely less on prediction and more on superior analysis of the present moment. If you share this feeling, you’ll agree that it’s hard to find a long term winner. This is where having superior valuation skills can offer an edge.

I’ve done a couple of posts on the fantastic bookExcess Returns, and what follows is going to be a few excerpts from that book. The author provides a specific discussion on accounting adjustments. This is how we can better evaluate the present moment. Let’s go through some adjustments we might want to make to gauge a clearer picture of what a business is worth in the present moment. It won’t be exhaustive, just some key ideas.

Shares Outstanding

The author, Vanhaverbeke, writes this:

If the company has convertible bonds, options and/or warrants outstanding, it is best to include those that are likely to be converted into common stock in the number of shares. Referring to the fact that the share base is likely to be diluted in the future due to this conversion, the resulting P/E is called the diluted P/E.

Free Cash Flow

Free cash flow is an easily distorted metric. When using it in your valuations, you’ll want to check out what the business is spending on maintenance and what on growth.

Reported free cash flow figures will be after maintenance and growth costs; it’s easy for a company that’s investing heavily into growth to look expensive. If we’re to prevent punishing companies that are investing for growth, we’d add back growth capex into the free cash flow figures.

Enterprise Value

The enterprise value (EV) is the net amount an acquirer would have to pay for the company after retirement of all debt and the sale of all equity investments in which the company has a minority stake. In case the company has subsidiaries one should use the proportionate share in the debt, cash, and equity stakes of these subsidiaries.

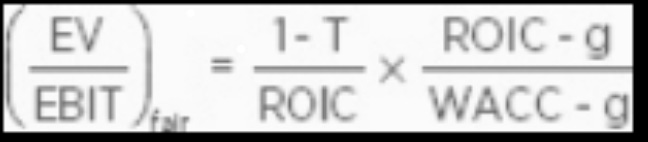

To calculate a metric like EV/EBIT, this is the formula Vanhaverbeke recommends:

In the demoninator we put the pre-tax earnings that the acquirer would get from the company when all debt is retired (i.e., when there is no interest expense left) and when all excess cash is used to pay for the acquisition (so there is no interest income). This is EBIT where the implied interest expense on operating leases is added back (because it is an interest expense that would no longer be there if the operating leases were settled), and where adjustments are made such that only the proportionate share of income of the majority holdings (and not the entire consolidated income) is included.

For instance, if we’re to find the fair EV/EBIT multiple, we might go about it like this:

Assuming a constant growth rate g, a constant ROIC, and a constant WACC, it can be shown that the fair EV/EBIT is:

Where T is the tax rate. This expression illustrates that the fair multiple increases with growth only if the growth is sufficiently profitable (i.e., when ROIC > WACC)

I think that’s a very interesting way to approach a valuation: backed by reasoning and common sense.

Accounting Principles

Various companies, industries, and countries approach accounting differently. If we want to evaluate each effectively — we need to get an idea of how to adjust the numbers based on those varying accounting principles. Some rules can produce extremely unrealistic values of certain assets.

Vanhaverbeke gives a few great examples:

Adjustments to inventory: if the company uses the Last In First Out (LIFO) inventory accounting method, the reported inventory should be increased by the LIFO reserve to obtain a more realistic value.

Marking to market: some assets (e.g., long-lived assets like land and bonds) should be marked to market as they are reported at a historical cost that may significantly misstate their current value. Marking to market can become very important if inflation has been high since assets were purchased. Note that also the book value of debt should be replaced with its market value as a buyer would look in the first place to the market value of the liabilities.

Adjusting for unrealistic depreciation: depending on the depreciation method and the asset, accounting depreciation may have little to do with economic depreciation. Therefore, proper adjustments are recommended to bring depreciated assets closer to their economic value. For instance, depreciation for real estate is usually meaningless as most real estate tends to appreciate rather than depreciate in value. Or an accelerated depreciation method may reduce an asset’s book value to much below what it is really worth.

Adjustment for hidden and off-balance sheet assets: although a conservative valuation assigns no value to goodwill and intangibles, it is sometimes recommended to add certain hidden or off-balance sheet assets to the liquidation value. For instance, there can be interest in a valuable brand or in R&D in a liquidation sale.

Adjustments due to market conditions and selling pressure: the market conditions (e.g., business cycle), competition among bidders (or lack thereof) and the pressure under which the assets have to be sold in a liquidation can have an important impact on the price that is ultimately paid for those assets.

After adjustments due to accounting principles, it is therefore recommended to make the following (downward) adjustments to the estimated economic value of certain assets, based on an assessment of the conditions under which the assets are likely to be sold:

Adjustments for sales under duress: if a company has to sell its assets under duress (e.g., due to a high debt load that becomes due soon), the cash collected for the assets is bound to be much lower than when the company has the time to look for the best bidder.

Vanhaverbeke goes through heaps of methods that we haven’t discussed today, I’ve only chosen those most I believe to be most important. If you want to see more on book value, net-nets, liquidation value, EV/FCF, earnings power value, and more — check out the book (Excess Returns).

This is a game of probability.

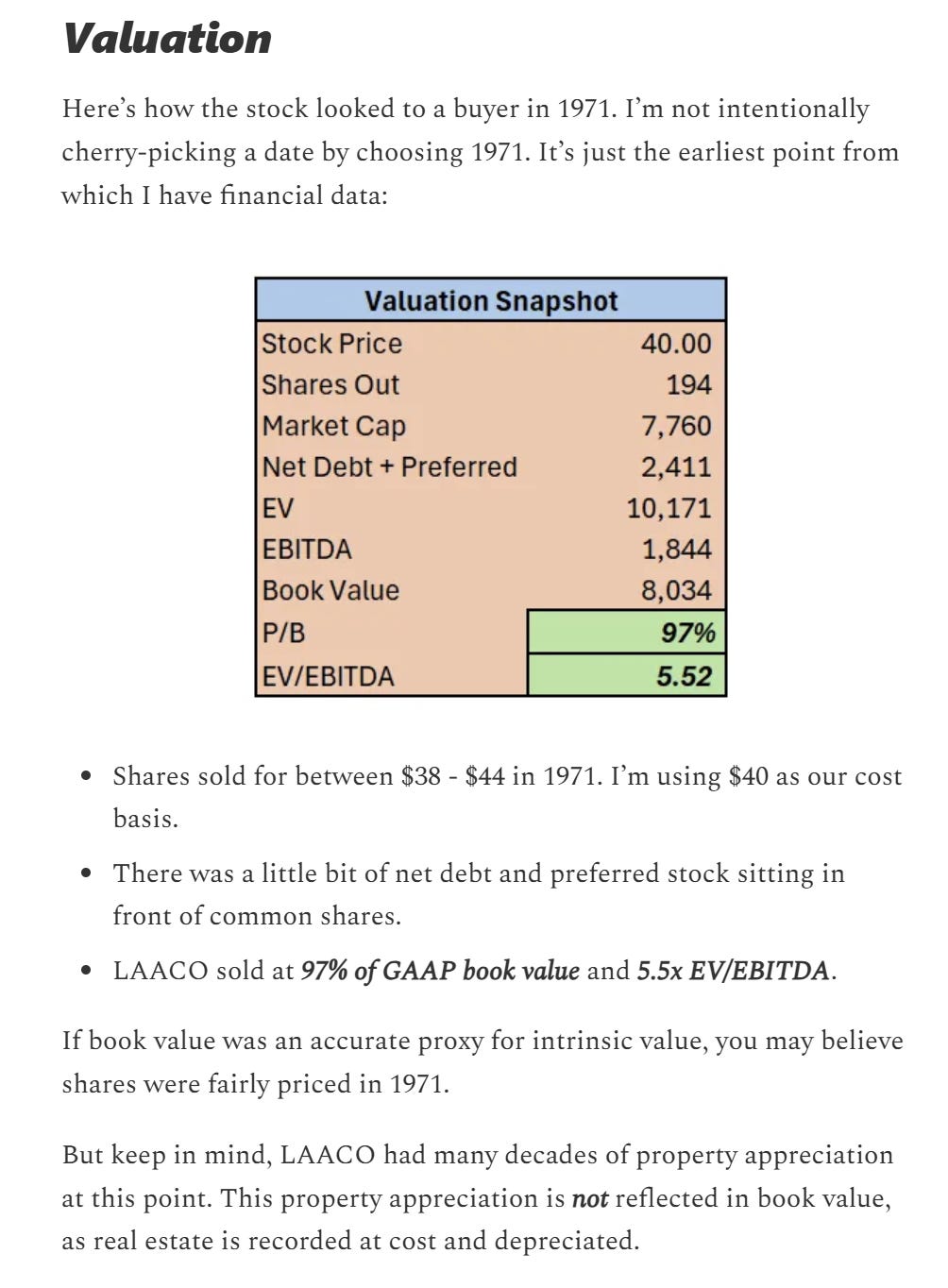

Investing is a game of probabilities, we must do what we can to tilt the odds in our favour, simplicity is one of those things. A writer I admire on this platform is Dirtcheapstocks, he pitches investments without jargon and simple numbers. Recently, he did a great write-up on an old business called Los Angeles Athletic Club, (LAACO), the image below is a snapshot of part of the write-up.

Source: Dirtcheapstocks

There’s something about a two-column Excel table that I love... To communicate a stock pitch in a few cells is as simple as it gets.

When less needs to go right for you to make money, you rely more on analysis than on luck and prediction in creating wealth. You’ll miss a few big winners by avoiding the overly complex stuff, but you’ll also miss a lot of losers. And that’s the aim of my game: try to avoid downside and let the upside take care of itself…

This simple approach does have one drawback. It doesn’t make you feel very smart. But always remember that as Charlie Munger would say, simplicity is what comes at the end of a long journey toward understanding.

If you’ve ever cringed at a simple piece of advice and eventually found yourself agreeing with it, that signified the end of your journey toward understanding. For instance, growing up you’re told that money won’t make you happy; you pass it off as something that doesn’t apply: ‘money most certainly will make me happy!’ You say.Yet every billionaire always says the same thing: it doesn’t do squat for happiness. It enables many happy things, but money itself brings nothing. You only realise the truth in that simple statement after a lifetime of understanding. So next time you pass off something simple as cringe/wrong, take a moment to think whether you’re saying that because 1) it’s wrong, or if 2) you haven’t reached the level of understanding to appreciate it fully.

This brings my mind to the idea that simplicity is the mark of genius.

It is the sign of a charlatan to make a simple concept complex, it is the sign of a genius to make a complex concept simple.

- Albert Einstein

When you fundamentally understand something you can explain it in a few words to a child — that kind of simplicity is a sign of true understanding.

That’s why I think simplicity wins. I think a humble forecast, a well-adjusted TTM valuation, and a good degree of conservatism is a sign of great understanding, of humility, and it’s a strategy with a great appreciation for randomness and probabilistic thinking. To achieve simplicity is not to be overly simplistic, it’s to have a critical understanding of what’s important.

Also, the beauty of markets is that we can — and even should — disagree with each other, we all have different areas of expertise and so forth. If everyone agreed with one another, the market would literally fall apart. So if you disagree with me today, it is not that either of us are wrong, it is simply that we do not agree.

Do bare in mind that I’m still young and my ideas adapt as new data and experiences arrive; this is how I view the investment process based on my own skill set and from my observations of investors I most admire. Do what works for you, and if you’re unsure what works for you, hopefully this article helped.

Thank you for reading.

Sincerely,

The Intellectual Edge.

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.

does not constitute financial, investment, legal, or professional advice. While every effort has been made to ensure the accuracy of the information, no guarantee is given that it is free from errors or omissions. The author accepts no responsibility or liability for any loss, damage, or harm arising from reliance on this content. Readers should conduct their own research and seek advice from qualified professionals before making any decisions based on the information provided

Thumbnail: Monk by sea, by Caspar David Friedrich — 1809

Yes, keep it simple. Do less, do it better. What is the worst thing in your portfolio? Why not just sell it?

Simplicity contains the power to protect your potential. It wins the ultimate battle against distractions.