A Story of Illusion, Greed, and Madness

The Great Crash 1929 - J.K Galbraith

Why do financial crises keep happening, even when the warning signs are obvious?

Everyone sees the excess. The speculation. The unsustainable euphoria.

Yet time and time again, the people who should act don’t.

Why? Because the greatest threat to capitalism isn’t external. It’s internal, woven into the incentives and psychology of those in power.

This is the story of the Great Crash of 1929. A book by J.K. Galbraith that covers the crash that sparked the Great Depression.

Today, I will break down everything we need to know.

The Calm Before The Storm

“The striking thing about the stock market speculation of 1929 was not the massiveness of the participation. Rather it was the way it became central to the culture.”

J.K. Galbraith

Picture this, you are in New York in the roaring 20s, opportunity is vast, the stock market is creating millionaires overnight, cab drivers, teachers, farmers, dentists, all gambling on the stock market like it is a sure thing, discussing their genius investments at dinner parties.

You walk into a barbershop, and the barber is giving you stock tips.

Everyone believes they are experts, it isn’t just a good economic environment, it is a mass psychological event where optimism has been grossly detached from reality.

People believe it is their eternal right that they deserve to become rich, and they want it fast.

There is a great demand to get rich quick, and so, thanks to the laws of economics, the supply of opportunities to get rich arrive in their masses.

One of these opportunities arose in the form of the investment trust, an opportunity for the retail investor to invest in a broad range of stocks that he could previously not attain, a truly revolutionary creation.

Hopefully you now see the position these people were in, they had no cause for concern, opportunities were rising like weeds, gleefully grasped by anyone who got there first. The investment trust was no different, it was adopted en masse.

Innovation Taken Too Far

Just like any good idea, someone had to ruin the fun and take things too far, investment trusts became ticking time bombs. Managers wanted more returns, so they employed leverage.

Some managers, with their leveraged money, invested in leveraged investment trusts, which layered the leverage and amplified returns to astronomical levels.

The chaos caused by the layering of leverage in a financial instrument was not isolated to 1929.

Let’s look at the 2008 Financial Crisis.

The CDO, like the investment trust, had the capability of causing harm, but nothing that could cripple an economy, until synthetic CDO’s were created.

These were packages full of low quality mortgage backed securities, and once deemed as diversified, labelled as investment grade.

This layered nature of investment into mortgage backed securities eventually meant that when mortgages defaulted, institutions could lose 10’s of billions of dollars despite the value of the underlying mortgages being say, 1 billion dollars. This is why the 2008 crisis was so catastrophic.

If that sounded all a bit too much - here’s an analogy: Dan has a $10 loan, Jim thinks he will be able to pay it back, so Jim bets $50 with Amy that he will pay up. Sophie thinks Jim will win his bet, and bets $300 with Dan over it.

Dan didn’t pay up his $10, and Jim and Sophie lost $350 combined.

That is how a $10 loan can be responsible for $350 of risk, and that is what happened in 1929, and 2008. Only on a scale so astronomical that it crippled America both times.

A good idea, taken much too far.

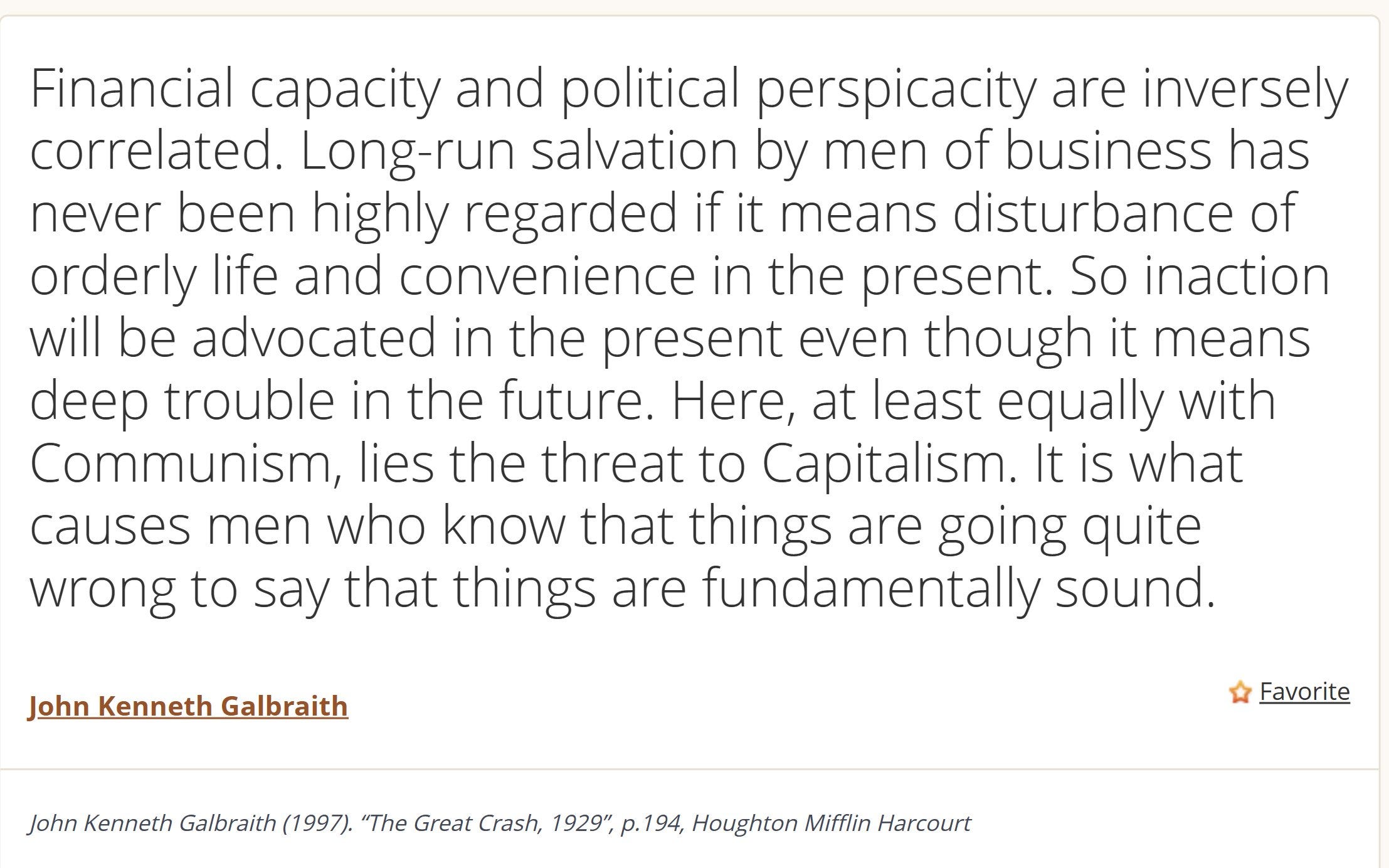

The Anatomy of a Bubble

"Perhaps it was worth being poor for a long time to be so rich for just a little while"

J.K. Galbraith

Markets aren’t just numbers, they are made up of people, and if people are not rational - It is fair to say then that markets are irrational.

1929 Is one of the times in history where markets became particularly irrational.

It was a roller coaster of a year, and everyone wanted a seat.

But the roller coaster of the 1929 bubble had an expensive fair.

This ride promised people riches, it promised them a touch of the good life, a glimpse into the 1%, their friends were getting rich, they wanted to feel the sensation, the pride, the snobbery that came with possessing money.

They wanted a seat on this ride so desperately that they paid for it with an entire decade of pain; sacrificing happiness and prosperity to momentarily experience the futile beauty of riches.

This delusion, that the value of this ride was worth their life savings, was one of the key ingredients that made the crash so catastrophic to the American people; this is one of the hallmarks of a bubble: when risk is replaced with certainty, and individuals pile in because they believe there is no way to lose money.

This Mark Twain quote seems appropriate:

“It ain't what you don't know that gets you into trouble. It's what you know for sure that just ain't so”

Mark Twain

Another hallmark of a financial bubble is the sudden belief of invincibility, the idea that we have finally outsmarted history.

Human nature is inevitable, it sneakily reveals itself in different forms.

People will feel they have outsmarted history by fixing the holes that previous generations punched into the wall of time, forgetting that there is plenty of room for the future to punch more holes. In patching up each hole, we get smarter, but our human nature is the hole punch - and we can not destroy that; Therefore, we must learn to live with it and prepare for more holes to be punched, at any point, in any place.

The idea that this time is different is yet to be proven fruitful, in 1929 people held strongly the idea that the fun could never stop, in 2008 people thought house prices will rise forever, in 2021 people thought the rising value of cryptocurrencies became an inevitability. Notice how our mistakes are all caused by the same underlying idea that the situation now will carry on for the foreseeable future - this idea crops up in different forms, real estate, stocks, crypto, low interest rates. Change is inevitable, both for good and bad, and when we begin to believe that good is inevitable - that sparks cause for concern that we are entering bubble territory.

Another hallmark of a bubble: the smartest people in the room leading the charge. In 1929, the President, the bankers, the Federal Reserve board, all of which would gleefully ignore warning signs and continuously tell people that ‘stocks are cheap’, ‘it has never been a better time to invest’, ‘keep buying, the economy is sound’.

These were the words being preached by the people in charge, these ideas are of course then adopted by those who seek advice, by those who do not know what they are doing, and by those who need authority to make choices.

Unfortunately, opinion and truth are not interchangeable terms.

If you asked a financial advisor what to buy in 1929, he would offer you a list of leveraged investment trusts; he would not tell you to avoid this chaos at all costs, if he told you that, he would make no money.

If you asked a mortgage broker to get you a mortgage in 2005, he would give you a mortgage; he would not tell you no, you will not be able to make your payments, if he told you that, he would make no money.

Noticing a theme? Incentives.

“Show me the incentive and I’ll show you the outcome”

- Charlie Munger

One of Charlie Mungers biggest ideas was the power of incentives, it is what governs this world, and it was takes a healthy market to a euphoric market.

As sad as it is, people are never truly looking out for one another, we are a species driven by incentives.

Think about evolution, the incentive was to stay alive, so we evolved.

Nowadays the incentives are not so black and white.

When money is involved - believing that someone wants the best for you is a risky belief, it may well be true, but that idea comes with a great deal of risk.

Every wise investor tells us that short term trading is a killer of returns, yet short term trading persists, why? Why have companies not listened to the most successful people in the industry?

Well, how much commission would Hargeaves Lansdown collect from you if you just bought a share and held it for 20 years? How about if you bought and sold that share twice a year for 20 years? They need short-termism to extract the most profit possible.

This is a piece of the puzzle that explains the prominence of trading, it is required for the profitability of brokers.

Here we are, with the greatest investors telling us the strong argument against short term trading, yet it persists. That is just how strong a force incentives can be, they overpower the very advice that offers us riches.

In every bubble, you will notice incentives playing their invisible but potent role in its creation.

The last hallmark that I will talk of is a combination of factors, leverage and the growth in prices outpacing the growth in value.

Leverage is a powerful tool, it makes good things great, and bad things awful. In every crash you see a vast over-extension of leverage. In 1929 it was to buy stocks, and in 2008 it was to buy homes. If you notice a sudden rise in leverage, beware.

The growth in cash flows among the businesses of 1929 was far outpaced by the growth in the price of businesses in 1929. This leads of course to overvaluation.

Since many of the participants were just average working people, they were blissfully unaware of the underlying value of their investments.

“Nowadays people know the price of everything and the value of nothing.”

―Oscar Wilde, The Picture of Dorian Gray

As Oscar Wilde says much better than I, people knew that something sold for $50 a share, they did not know it was worth $5 a share, they simply did not know what they were buying.

People left their circle of competence and got punished for it.

If one can not gauge a value of an asset, how can one possibly know a price at which is reasonable. This is a fact that people seem to forget when everything is going up.

A Slow Unraveling, Then a Sudden Collapse

"The end had come, but it was not in sight yet."

J.K. Galbraith

The market begun to wobble in early September 1929.

The warning signs were there, commodity prices falling, industrial production slowing, but no one wanted to believe it - they believed the good things had to be everlasting.

It is hard not to believe things are good when your President says things like this:

“The fundamental business of the country… is on a sound and prosperous basis.”

– Herbert Hoover, days before the crash.

Since so much of the investment at this time was built on incredibly weak foundations, it did not take much to bring it crashing down. What was needed to stop it falling was education, not advice.

October 24, 1929 – Black Thursday: A sharp sell-off. Panic sets in.

October 29, 1929 – Black Tuesday: The dam breaks. The illusion is shattered.

This short time period has so much insight for us. Taking a presidents word for gospel being an unsound activity is an insight one could postulate…

Thinking independently and gathering your own opinions allows you to reach the best conclusions, do not take other peoples word for gospel.

Why We Always Think ‘This Time Is Different’

The market collapsed in a brutal manner, no one was buying, some stocks selling at $12 had buy orders filled at $1 simply because there was no one buying, the desire to sell was sudden, and extreme.

Fortunes were wiped out immediately. Ordinary investors lost everything.

The Great Depression followed, this was not just an economic crisis, but a crisis of belief in the system itself. What started as a desire to become rich became a desire to survive.

This depression lasted an entire decade, and scarred its victims.

But here’s the thing: Even after 1929, bubbles continued.

Galbraith mentions how we are immunised to another crash by the memory of the last, once the memory of the previous crash fades, we lose our immunity and are vulnerable once more.

This is why crashes can seem eerily similar, but keep happening over and over again, if people forget, there is nothing to protect them from the same thing happening again.

One common parallel is that when a new bubble that surfaces, it is built on a story that feels undeniably true.

2000 – The Dot-Com Bubble: “The internet has changed the economy forever.”

2008 – The Housing Bubble: “Real estate never goes down.”

2021 – The Crypto-Bubble: “Decentralised finance will replace banks.”

What is fascinating is that each of these statements have undeniable elements of truth, it is only when the ideas are taken too far, that is how the issues arise.

Internet stocks were great investments, property prices have continued to rise, crypto is being adopted more by the day, these situations were deserved of the podium they were bestowed upon, it is that people took these ideas and believed that they could fly close to the sun with them and not get burnt.

It was not the ideas fault that we got burnt.

It is us, it is our gross misuse of brilliant ideas that force us to learn the hard way about things.

The Eternal Cycle of Human Nature

Galbraith finishes the book with something so profound that I will not paraphrase it.

When people are making money, no one wants to bring their head out of the sand and see how dire situations may truly be.

If individuals believe life to be good, people do not have the strength to tell them this life can not be sustained, so they sit and watch despite the inevitable trouble it brings down the road.

He says that capitalism is its own biggest threat, because the incentive system is built in a manner in which it periodically breaks itself.

This incredible insight is why we absolutely must expect, and prepare for, major crashes in the future.

What Can We Learn?

Crashes are not an anomaly. They are a feature of the system, we can not escape them, the system is built to crash, and we must prepare for this.

To succeed in the market, a knowledge of numbers is not enough; it is equally important to have a grasp on human nature, the madness of crowds, and standard human psychology.

The next crash won’t look like 1929, 1987, 2000, or 2008, but the underlying forces will be the same. You best believe that incentives will work hard in creating it.

This book cements the importance of being a contrarian, you had to literally stand up against the Federal Reserve and The President if you wanted to see clearly, how much more contrarian does it get? Individual, critical thought is the foundation that successful investment is built on.

My last lesson from this chaotic event will be the words from an investment legend,

“The four most dangerous words in investing are: this time it's different”

- Sir John Templeton

Thank you so much for reading, I hope you learnt as much as I did, I couldn’t recommend this book enough, it was such an enjoyable read.

Please let me know your thoughts on this incredible story, I would love to hear from you!

Sincerely,

The Intellectual Edge